Written by UPA, Urban Property Australia

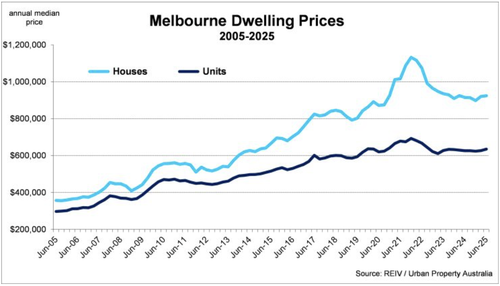

Melbourne’s median house price increased for a second consecutive quarter, for the first time since 2021 with Melbourne’s house prices increasing by 0.4% over the quarter and 1.0% over the year;

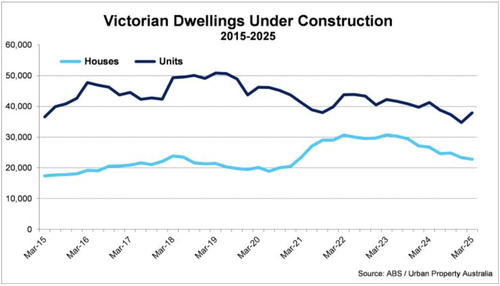

There are currently 60,700 dwellings under construction across Victoria, 11% lower than the activity recorded 12 months ago, with high-density apartment development down 8% and detached housing development 15% lower than last year;

While the vacancy rate for Melbourne residential property remains low at 2.5%, most sub-regions recorded increases of vacancy over the past 12 months.

Residential Market Summary

Melbourne’s median house price increased for a second consecutive quarter, for the first time since 2021, however remains significantly below their peak levels with current median house prices 18% lower than the highs of late 2021. The vacancy rate for Melbourne residential property increased to 2.5% compared to its rate of 2.2% a year earlier but remains below the 10-year average of 2.9%. Reflecting the low vacancy environment, metropolitan residential rents sit just short of the all-time highs achieved earlier this year with rental levels in the Regional markets for both houses and units sitting at all-time highs as at June 2025.

Prices

According to the REIV, Melbourne’s median house price increased for a second consecutive quarter, for the first time since 2021. As at June 2025, Melbourne’s median house price increased to $924,000 up 0.4% over the quarter and 1.0% higher than prices recorded 12 months ago according to the REIV. Melbourne median unit prices outperformed the detached market over the quarter and year with Melbourne unit prices having increased over the June quarter of 2025 by 1.3%, up to $635,000. Similar to the detached housing market, as at June 2025, the Melbourne median unit price has now exceeded levels recorded 12 months ago with current levels 1.4% higher than those recorded in June 2024. Currently, median prices of both Melbourne houses and units remain significantly below their peak levels with median house prices 18% lower and median unit prices 8% below their peak. Outside of Melbourne, the median Victorian Regional house price increased over the June 2025 quarter, increasing to $620,000, the highest quarterly increase since 2022. The median Victorian Regional unit price also increased over the quarter, rising to $430,000, but remains 1% off their peak recorded in 2022.

Supply

According to the ABS, there are currently 60,700 dwellings under construction across Victoria, 11% lower than the activity recorded 12 months ago, with high-density apartment development down 8% lower than levels recorded last year while the detached housing market development levels are 15% lower than the preceding year. Despite population growth close to all-time highs, the number of dwellings currently under construction in Victoria is 18% below its peak. The level of new dwellings completed in Victoria continues to decline, with housing completions now 3% than its 10-year average. Looking forward, supply levels are projected to continue to remain subdued with commencements also below their long-term levels with current commencements 15% lower than the 10-year average. The decline in the pipeline of housing stock is further evidenced by decreasing level of approved dwellings in Victoria with current levels 13% lower than the 10-year average. In order to encourage supply, the Victorian state government has recently announced two policies that aim to give developers an incentive to build. Firstly, stamp duty was reduced from October 2024 and be in place for 12 months and available for off-the-plan units, townhouses and apartments for properties at any price point. Secondly, to encourage more density around railway and tram lines, the government has identified 50 new activity centres where the planning process for multi-storey residential dwellings will be streamlined to fast-track development.

Demand

Despite down on record high levels, Victoria’s population continues to grow by the highest level of any Australian state with Victoria’s population having increased by 132,500 people over 2024, driven by overseas migrants relocating to the state. Total quarterly Victorian housing finance commitments continue to gather momentum having trended upwards since 2023 and now sit 17% above the 10-year average as at March 2025 with $84.6 billion financed. Dwelling finance commitments have increased across all categories over the past 12 months. Non-first home buyer owner occupier finance levels have increased by 12% compared to the preceding year; with first home buyers also active with their levels 11% higher than last year. Investors now account for 31% of total housing finance commitments in Victoria, in line with the long-term average share of 31%. Looking ahead, with strong rental growth and a shortage of housing, Urban Property Australia expects that investors will grow their share of housing loans as affordability challenges restrict owner occupiers despite increases in land taxes.

Vacancy

According to the REIV, as at June 2025, the vacancy rate for Melbourne residential property increased to 2.5% compared to its rate of 2.2% a year earlier but remains below the 10-year average of 2.9%. All precincts’ current vacancy rates now sit below their respective 10-year averages; with the exception of the Outer region, however the majority of regions recorded increases of vacancy over the past 12 months. The vacancy rate of the Inner (4-10km) region recorded the tightest rate at 1.5%, up from 1.3%, 12 months earlier. The overall Inner Melbourne region (0-10km) holds the highest vacancy rate at 2.6% while the vacancy rate of the Outer region sits at 2.0% and the Middle region at 2.5%. Looking ahead, Urban Property Australia projects that the vacancy rate for the metropolitan Melbourne area will remain low with falling supply levels coupled with population growth of Melbourne currently expanding the fastest of all Australian states.

Rents

Reflecting the low vacancy environment, according to the REIV, metropolitan residential rents across the precincts increased (or remained steady) over the past year. Over the year to June 2025, the weekly median rent for houses in metropolitan Melbourne remained steady at $580 per week, just short of the all-time high of $590 per week. Across Melbourne, rents for houses located in the Inner region increased the most, increasing by 5.3%, with rents in the Middle and Outer regions both remaining steady. Melbourne units recorded stronger rental growth with annual rises of average rents increasing by 5.5% over the year with all precincts recording rental growth for units. Looking forward, Urban Property expects that residential rents will continue to rise, however the growth rates will moderate, as witnessed over the past year as affordability pressures begin to impact capacity of renters to absorb the significant growth observed in recent years.

Regional

The median Victorian Regional house price increased over the June 2025 quarter, rising to $620,000 – however remains below its peak recorded in 2022. The median Victorian Regional unit price also rose over the quarter, increasing to $430,000, and similarly remains below its peak level recorded in 2022. In contrast to the performance of median prices in Regional Victoria, rental levels in the Regional markets have remained resilient with the average weekly rental levels for both houses and units sitting at all-time highs as at June 2025. The vacancy rate for Regional Victoria remains very tight at 1.9%, below the metropolitan average of 2.5%.